Remember how this company Birchbox was everywhere 3 years ago? And how today it’s…not?

Turns out after raising $90 million at a peak valuation of $500 million, and after a few years of struggle, in 2018 Birchbox sold a majority stake to a hedge fund for only $15 million. This means after a journey of 8 years, its investors were totally wiped out. Employees who had exercised stock options came out with nothing.

Admittedly, I wasn’t a target customer, and this might have been obvious to their user base for years. But that this wasn’t bigger news (at least in the sources I read) reflects an ever-present survivorship bias in entrepreneurship. Successful companies soak up the attention; failed companies fade away with a whimper. We forget how much hype they built up years ago, and we turn our attention to the next hot thing.

But failed companies are where some of the best lessons can be learned. Warren Buffett says, “it’s good to learn from your mistakes. It’s better to learn from other people’s mistakes.”

Studying failed companies helps you better differentiate strategies that work from ones that don’t. Studying failed businesses helps you look past platitudes like “culture is everything” to understand the fundamentals of why a business failed. Studying failed startups helps you discount today’s breathless press hype, and better try to predict the future.

I’ve done a deep dive into 59+ failed startups. Each has a meaningful story to learn from.

- Most of these were venture funded by big names: Andreessen Horowitz, Sequoia, Kleiner Perkins, Accel, Greylock.

- They raised on average 8 figures of funding, some with $100 million+ – these were serious contenders, once strongly believed in by professional investors whose job it is to pick winners.

- Many of them have insightful postmortems written by a founder, complemented by third-party analysis of why the startups failed.

I hope they’re as useful to you as they were to me.

Introduction

The nominal reason why startups fail is they run out of money. The nominal reason startups run out of money is that there aren’t enough customers willing to buy the product to continue funding operations. As Paul Graham says, “there’s just one mistake that kills startups: not making something users want.”

But why? Why did users not ultimately want something that initially seemed like such a good idea? What caused the business (and investors, and the public) to mispredict what customers wanted, were willing to pay, or how many customers there were? In what cases were there mistakes in execution vs fundamental strategy problems?

Probing deeper into why individual businesses fail, you get more meaningful and actionable reasons:

- often your product doesn’t deliver enough value to warrant being paid for at all (as in healthcare and reimbursement by payers)

- sometimes there are easy, low-cost substitutes for what you’re producing (on-demand food industry)

- sometimes people see an industry as a commodity, and aren’t willing to pay more for better service (airline seats, moving company Walnut)

- sometimes you bet on a higher LTV for a subscription business than what you’ll actually get (Birchbox)

- sometimes you lose in network effects, causing a vicious cycle (Vid.me)

- sometimes the product costs way more per unit than you expected (many hardware companies)

- sometimes you’ve raised too much debt – you could have been sustainable, but the bank demanded loan payments that sunk the company (GigaOm)

- sometimes you get out-executed by a competitor; sometimes even despite the best execution, the entire industry is doomed to failure.

There are many reasons why startups fail. My aim was to find patterns that would help me better predict which projects will succeed.

For a vitally useful framework on how to understand markets, read Understanding Michael Porter.

About My Failed Startup Notes

This is clearly not an exhaustive list of failed companies, so be aware of my own selection bias. I focus on industries I care about – mainly consumer, some healthcare. I ignore entire problematic sectors like crypto/blockchain. I focus on companies that had meaningful traction, often venture-funded by big names to 8- or 9-figures.

I don’t cover some common reasons of why startups fail. For instance, I don’t cover startups that failed because of founder conflicts or failure of early execution (eg can’t get a product out the door). These are table stakes, and companies that fail this don’t make it deep into funding stage.

I don’t cover heavily technology-risk companies (eg pharma, medical devices, new energy tech), since the lessons aren’t as generalizable. In these cases, if they get the technology to work, there’d be a massive market demand. For most other businesses, the market demand is the tricky and mysterious part.

I try to get an objective, rounded view into why the company failed. Much of the info comes from very useful postmortems by founders – they usually have strategic insights into their failed startup that the public doesn’t. Third-party sources and customer perception help round out the picture.

Some of these “failed” companies were not outright failures (eg being acquihired), but they all represent disappointing endings from their original promise.

The investors listed are usually just the marquee names from a list of many investors.

I intend to update this periodically as we learn more about companies that failed.

Lessons from Failed Startups

Despite the very many unique reasons each company failed, here are lessons I’ve learned from these failed businesses:

- The market has evolved to be the way it is. Respect that and be worried about it. Don’t be sucked in by the Siren’s call of “this industry is massively fragmented/inefficient, the incumbents are dumb dinosaurs. I’ll be able to dominate through software/a superior UX.” The market is the way it is through decades of harsh competition. Understand exactly why the market is the way it is, before you muse about why you’re going to be so paradigm changing.

- Home cleaning, restaurants, elderly home care, tutoring, used car sales all look like fragmented local markets begging for a tech company to dominate and be a major player. It turns out, in all these fields, buyer preferences and incumbent power have shaped the industry to be exactly how it is, and technology is not as valuable as you might think.

- Small local incumbents have the advantage of needing lower margins than a larger company. It’s not easy to get people to pay for more in many industries.

- Quirky – the large gadget incumbents aren’t dumb. They may be slow to launch, but their research tends to work.

- Pay attention to unit economics. Don’t scale too hard without good understanding of potential for profitability.

- An unknown LTV makes this calculation difficult. Understandably, sometimes you have to swing for the fences or risk being outpaced by a competitor.

- Be very wary of customer willingness to pay, if you’re getting growth by selling dollars for 85 cents. Once you raise cost, your churn will go up.

- This gets worse in heated trendy markets, which attract a lot of competitors, driving CAC up and prices down. This makes figuring out a long-term sustainable model difficult.

- On-demand companies and food companies learned this lesson the hard way.

- Raising too much money can lots of problems: lack of discipline on spending, premature scaling in team or marketing, wasting money to get growth when funnel is broken, (more insidiously) growing at the expense of your original value prop that made you unique. This spend leads to sunk cost, making you more committed to your approach and less agile. Be more conservative until you nail product-market fit.

- Failed startups Airware, Moz, Gigaom, Fab.com, Nasty Gal all faced elements of this.

- The entrepreneurs’ paradox: if entrepreneurs didn’t really believe in their ideas, they would never take the huge risk to start their companies. But because of this conviction around certain success, they overextend.

- Listen to advice from domain experts and how they do things. Don’t be too arrogant.

- Failed startups Homejoy, Shyp both got advice that could have saved their companies had they pivoted earlier.

- If retention is important for your business, drill down on that before acquiring more users.

- If you’re essentially doing regulatory arbitrage, be wary that regulation can close off the wild west fun times.

- 1099 classification issues for on-demand gave them lower prices at first, until this was banned.

- Wonga was profitable with payday loans, until FCA regulation in the UK stifled practices and required restitution.

- If your company relies on network effects, you risk getting outcompeted by larger companies/incumbents and never getting a chance to return.

- Failed social startups Vid.me and App.net, and marketplace startup Wimdu.

- You may have a large viral hit, but they can bleed out quickly if the novelty wears off, or you compromise your value for the sake of growth.

- Failed startups Formspring, Yik Yak, HQ Trivia all had a huge growth spike, but later lost their users as reality hit.

- Hardware is hard. Anything involving atoms is also hard. The margins are lower, production runs into more issues than you would imagine.

- Failed startups in hardware (Quirky, Doppler Labs) and bits-to-atoms (food, on-demand services) found the economics impossible to overcome.

- Beware of too much positive feedback that aren’t actual sales.

- Beware of when people compliment you on the idea because it’ll be useful for people other than themselves. “This will be SO useful for [target segment.]” Don’t assume they’re right just because you heard it!

- Don’t ask about future behavior (“would you buy this”) but about past behavior (“when’s the last time you cooked something new?”)

- Validate before you build. Failed healthcare startup Driver spent 4 years building a pipeline to handle cancer patient biopsies, but expected consumers to pay $3k out of pocket. It launched and shuttered 2 months later.

- “Build it first, monetize later” has fallen out of fashion (as of mid 2010s). Now investors want more discipline around your path to profitability.

- This should be obvious, but the failure rate for even the top-tier VC firms is very high. Don’t see their vote of confidence as a minting of success. These companies may very well fold in 5 years.

- Likewise, be wary of breathless hype from press about a startup, whether it’s a company you want to fund, join, or compete against. Most of the companies on this list were once raved about, with their critical flaws unclear until well later.

Consumer

e-Commerce/Fashion/Clothing

- Monthly subscription box for cosmetics. Meant to personalize.

- Raised $87MM. Investors: Accel, First Round.

- Founded 2010. In 2018, Viking invests $15MM to get majority stake. Down from valued at $500MM. Investors wiped out.

- $10/mo subscription box was a big hit and spawned a wave of subscription box competitiors. But it wasn’t defensible – got stiff competition from Ipsy, Sephora, Allure Magazine.

- The ultimate goal was to buy full-sized versions of products at Birchbox. But customers had no particular reason to buy from Birchbox and not from Sephora/Ulta.

- Experiments to open retail stores failed.

- Product began suffering with poor customization.

Bonobos

- [Far from outright failure, but lower than their original ambition.]

- Raised $128MM. Sold to Walmart for $310MM

- Andy Dunn: “It’s a weird time to be a retail company. If you’re not Nike or Under Armour, or one of these really big vertical brands, or Chanel, or have tens of billions of dollars … it’s hard.”

- Design-focused flash sales model. Originally home decorations, then into more categories like furniture, jewelry, gadgets.

- Founded 2009. Acquired by PCH for ~$15MM.

- Raised $336MM. Peak valuation >$1B. Investors: Andreessen Horowitz, Tencent, Sherpa.

- Had a decently working model, but scaled up too quickly without fiscal discipline.

- Expanded prematurely into Europe to fend off copycats. Cost $60-100MM.

- Fab scaled up SKUs from 1k to 11k within 6 months. This made it lose its curated design feel, becoming more like a generic retailer.

- Retention was poor as they scaled up marketing.

- “Don’t ever allow yourself to slip into thinking, ‘We figured it out,’ or you risk losing it all,” Goldberg said. “It is very hard to remain humble when you are piloting a rocket ship. It is very hard to remain humble when the world is telling you: You are winning.”

- Fashion brand, based around Sophia Amoruso’s “elegant with a sexy edge” image.

- Founded 2006. Closed 2016, sold to Boohoo for $20MM.

- Raised $65MM. Investors: Index Ventures.

- Revenue hit $24MM in 2011, $100MM in 2012. But started dropping: $85MM in 2014. While Forbes estimated $300MM in revenue in 2015, it really had $77MM.

- Heavy spending in marketing, but not the retention to match it.

- Product quality was lacking – Zara and H&M offered strong competition.

- Costly, unprofitable extensions into larger offices, fulfillment centers, brick and mortar stores.

- Founder may have stepped off the pedal, caring about her personal brand more than rescuing the company.

- “The enormous valuations mean that the brands suddenly had to scale very quickly, which generally means no longer serving the needs of the customer originally drawn to the brand, but creating a blander product and brand experience that will appeal to a much wider segment of the market.” Nasty Gal head of PR

- Personalized gift recommendations for people. Moved into recommendations for the user herself.

- Founded 2011. Closed 2013.

- Raised $6MM. Investors: Polaris, Greylock.

- Insufficient growth to secure new capital.

- Personal e-commerce aggregators competed with Wanelo, Wish, Polyvore.

Marketplaces

- Used car marketplace, with company serving intermediary functions (inspection, cleanup, managing sale, delivery) for a 9% commission.

- Vision was to build a trustworthy brand to counter the risk of used cars.

- Raised $150MM. Investors: Yuri Milner, Sherpa, Redpoint.

- Its practices may not have been defensible from local used car incumbents, and online players like CarMax and Autotrader.. Began offering the same perks as Beepi.

- Fiscally irresponsible

- Burned $7MM a month. Abuse of funds for personal uses claimed.

- “They were running the business to raise money, and then to get someone else to take it on”

- [There’s more to the fundamentals here that I haven’t seen, like buyers not wanting to buy cars sight unseen, which would drive power to local players.” They had good Yelp reviews so their service wasn’t terrible.]

- Rocket Internet’s Airbnb clone. Better funded at first (threatened Airbnb: acquire us or we’ll stomp you), then Airbnb raised.

- Failed to grow house inventory at scale. (Possibly lost the network effects virtuous cycle)

- In 2016 merged with 9Flats, then got acquired by Novasol (Wyndham), then to PE firm Platinum Equity for $1.3B. Then finally shut down as transition

On-Demand (Uber for X)

The best breakdown of Uber for X on-demand companies comes from Y Combinator.

- In general: the more customization needs to happen in a match, and personal preferences play a role, the less an edge software provides.

- Uber worked because car driving is super commoditized, thus decreasing supplier power and threat of distintermediation; plus its on-demand, specific-location nature gave technology a big edge over incumbents.

- For consumer side, consider where the task is on the skill vs demand frequency axes

- The less complicated/specialized the task:

- the more commoditized it is, the more servicers are interchangeable and customized matching is less important. Less screening is needed for quality and the right fit

- For highly customized needs like plumbing or childcare, the rest are the opposite. This makes Uber like model less tenable, as it requires more customization, upfront understanding, and communication

- For less frequent/pre-scheduled items (like plumbing, tutoring):

- Time urgency is less important. On demand doesn’t mean “now,” it means “when I want it” and thus annoying logistics and scheduling has to happen.

- Logistics matter – rescheduling, canceling, no-shows

- Do NOT assume that “instant” is the default behavior when booking a service pro. In fact you may need to support the logistics of rebooking recurring relationships.

- For highly specialized and less frequent items, consumers would rather reschedule people they already know

- This can lead to disintermediation, and give less of an edge to technology.

Common threads:

- More difficult unit economics than expected.

- If a skilled service (like housecleaning), best performers disintermediate and strike direct deals.

- Vicious cycle of poor quality contractors -> lower customer retention -> less money to pay -> poor quality contractors

- Good local incumbents with reputations already there.

- People less willing to pay for convenience and time than expected

- Regulatory issues with 1099 misclassification

Blackjet

- Charged annual fee ($15k) for access to network of private jets, on which they could book seats on pre-determined routes.

- Raised $3MM. Investors: First Round, Garrett Camp, Tim Ferriss.

- Heavy regulation: FAA doesn’t allow you to take paying passengers automatically just because you own an aircraft. More on this

- Lot of other companies in the space.

- Personal errands on demand. Ubers meets Taskrabbit (a faster lower-friction form of getting help).

- Founded by Justin Kan of Justin.tv (Twitch) fame in 2011. Closed 2014

- Raised $3MM. Investors: SV Angel, Y Combinator.

- Execs would show up in track jackets and do whatever you wanted – dog walk, bartend, move your car.

- To make economics work, had to hike rates to $30/hour and 10% surcharge. Eventually had to shut Errands down. Problems with:

- Hiring: “Most competent people are not looking for part-time work. Hiring new errand runners was expensive, and it was difficult to get them to stick around when we couldn’t guarantee work.” Had 50% utilization.

- Meeting spiky demand – without surge pricing, hard to get enough supply side.

- People not having errands to run – low activation rate.

- Interestingly, servicing their own jobs (sending employees to do tasks) gave a false sense of quality, since competence of employees was higher than contractors.

- Cleaning was working, making up over 50% of orders and 90%+ hours by Execs. Became $89 for basic 1BR/1BA job. Acquired by Handy in Jan 2014.

- On-demand home cleaning.

- Founded in 2010. Closed in 2015.

- Raised $66MM. Investors: First Round.

- Mounting losses, poor customer retention, a costly international expansion, run-of-the-mill execution problems, technical glitches and the steady leak of its best workers to direct employment arrangements with its own (now former) clients

- High CAC giving away service without retention

- Only about a quarter of its customers continued to use the service after the first month, and less than 10 percent used it after six months.

- In some of these regions, the competition for cleaners from well-established professional cleaning services, like MerryMaids, was fierce.

- recalled a persistent issue that took a backseat to growth. For months, the person said, the founders failed to resolve a flaw in the algorithm, which set up back-to-back jobs for cleaners without accounting for the transit time.

- Cleaners who excelled would sometimes strike independent relationships with clients who wanted to see them again

- Homejoy’s general approach to maintaining quality was to try out cleaners for a period and then boot them off the platform if they didn’t work out.

- Last-minute cancellations were a particularly vexing issue for the customer and client services teams, as Homejoy could typically only find a replacement about 15 to 20 percent of the time, according to a former employee. The problem was that in many of the largest cities, Homejoy didn’t reach a critical mass of cleaners. With short notice, it was difficult for most cleaners to travel across town to make an appointment on time.

- “Advice often wasn’t heeded,” the former employee said. “There was a great deal of arrogance, especially after they [founders] secured the money.”

- Little experience in customer support or home services

- Adora claims worker classification was the killer. Commenters not sure this was the major reason

- Cleaners require a higher level of training, and most can make more money by running their own business. [For Uber, driving a cab putatively needed a cab license. Not having one made it hard to advertise your services and be trustworthy.]

- Sources say [CFO] Vranesh left after it became clear that the company would not be taken public.

- Childcare agency (directly managed employees rather than having contractors).

- Unit economics didn’t work in directly managed childcare model

- On-demand shipping service. Pickup, pack.

- Founded in 2013. Closed in 2018.

- Raised $62MM. Investors: Kleiner, Sherpa. Peak valuation: $250MM

- Consumer product slowed down. Got advice to chase SMBs, but founder didn’t heed advice. SMB-focused businesses Shippo and Shipbob are still alive.

- Cut burn too late, kept popular but unprofitable lines running. Had a $5 pickup fee for a while, regardless of packaging used and size of items.

- Was able to negotiate discounts with UPS with volume.

- Good history

- [Small company, put here for the insightful postmortem on their industry.]

- Operational efficiency and seasonality putting upward pressure on costs

- Ton shows how scheduling steady hours, offering benefits, and investing in training can lead to operational efficiencies that more than cover the added employee costs.

- [But founder says moving is more random situations, less predictability and so less return to training]

- Seasonality is trad. managed by firing workers in off season or subcontracting.

- To offer good jobs—and be the employers we aspire to be—we can’t manage seasonality this way. More importantly, we also don’t want to lose our best employees during slow season. So is it possible to offer good jobs at all?

- Our no tipping policy made us less competitive, not more

- We later learned that this policy relied on a false assumption that customers would evaluate the sticker prices of their moves with Walnut against the total costs of moves with our competitors. We found that they didn’t, and that tips on moving day might even be considered a completely different expense.

- Creating a better experience for customers and employees wasn’t sustainable. We were paying our employees higher base wages than competitors, and our customers were evaluating our all-in prices as more expensive than the pre-tip quotes that they were receiving elsewhere.

- [At the end of the day, buyers weren’t willing to pay more for better service.] What we found was that while many people complain about their moving companies, even the highest income consumers would not pay for a better service. Our mistake was conflating desire for a better product with desire to pay more for a better product. It’s hard not to choose the company offering the lowest price.

- Even a low NPS may not be indicative of a good business.

- Moving happens once a year at most, and humans are hardwired to forget distant pain.

- For discretionary purchases — hotels, clothing, cars, restaurants — people splurge to get a tangible upgrade. For compulsory expenses — a flight, a move, or parking — they skimp as much as possible.

- Think about the last time you parked at a venue for a game or concert. Driving around, you notice that the lots charge slightly more the closer they are to the entrance. Without questioning it, we’ll park a fifteen minute walk away to save $5 on parking (a compulsory expense), then spend $60 dollars on beers and bad nachos inside!

- The future depended on transforming bad unit economics. History doesn’t look favorably on this strategy.

- On-demand dry cleaning and laundry.

- Founded in 2013. Closed in 2016.

- Raised $17MM. Investors: Sherpa

- Grew to 7 cities.

- Economics were tough. Charged $2.19 a pound for laundry, and $6 delivery fee.

- Intense competition from other competitors like Rinse (still alive)

- Virtual assistant matchmaking.

- Founded in 2011. Closed in 2015.

- Raised $6MM. Investors: VegasTechFund, Jason Calacanis.

- $11MM run rate, burning $400k a month.

- In short, their burn rate was higher than expected, and they couldn’t raise another round to keep going.

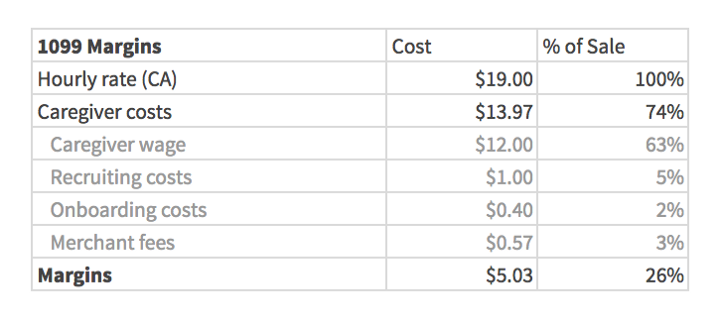

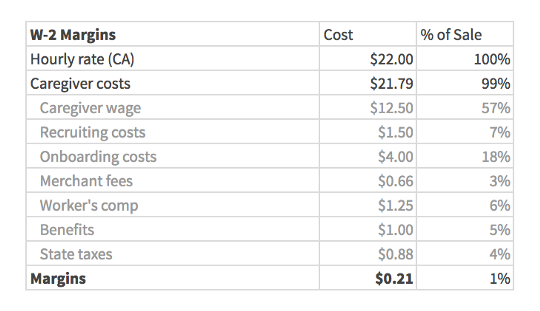

- Moved from 1099 to W2 (apparently voluntarily). Margins were obliterated (add on 20-30% to contractor cost).

- Founder blames outside CFO service for error in omitting two payroll cycles. When this was noticed, they scrambled to get bridge funding, but couldn’t.

- Founder says she should have hired a senior finance and ops person earlier, instead of trying to save money.

- In failure to fund raise, they couldn’t make payroll and had to shut down, meaning all clients also lost support.

- Startups.co acquired Zirtual and continued operations.

- Fundamental: the business was tough to begin with.

Hardware

- Wireless earbuds, founded in 2013, competitor to Airpods (released in 2016). Features like audio transparency to outside, selective noise filtering. Wanted to have real time translations.

- Raised $51MM. Investors: Chernin Group, Accel, a few billionaires like David Geffen

- WIth prototypes, reasonably thought one of the big 5 tech companies would acquire them after meetings. “We thought we were the shit.” The companies liked the tech, but wanted to see Doppler massproduce a product.

- Before launch, their production models had problems. Low battery life, charging issues. Missed the holiday season and released after Airpods. Product flopped: 25k sales, rather than 100k expected.

- “We fucking started a hardware business! There’s nothing else to talk about. We shouldn’t have done that.”

- Cites Jawbone, Pebble, Juicero as high-profile hardware problems.

- Development of new consumer products. Crowdsource ideas, the best ideas get made and the contributor gets a share of sales.

- In more detail: ideas are pitched from public and contributors can suggest improvements. Quirky patents, manufacturers, and sells the unit. 10% go to inventor and to helpers.

- Execs also had livestream where best products were pitched and evaluated by experts.

- Raised $185MM. Investors: Andreessen Horowitz (A16Z), Kleiner, Norwest, GE.

- Launched in 2007, helped by recession-driven push for alternative incomes (same as Kickstarter and Shark Tank).

- Some products (like Aros, a smart air conditioner) were hits, earning the inventor $400k.

- But others were total flops.

- Wireless speaker Beat Booster cost company $388k but sold 30 units.

- In total Quirky brought 400 products to market in 6 years.

- Further, judging by Amazon reviews, the product quality wasn’t great. Wireless connection to IoT tools was clunky, poor battery life, etc.

- Fundamental: Crowdsourcing just didn’t produce enough good ideas. Amateurs green-lit solutions to nonexistent issues (large hardware companies may be slower to launch, but their research can work). Possible that the really great inventors would go the solo route, especially with decreasing cost of hardware prototyping. Also a longer-term risk that really good sellers will be replicated by low-cost manufacturers and incumbents.

- Kickstarter was a more sustainable structure, merely providing a platform for inventors and followers to connect, rather than taking on the risk of vertical production.

- Founded by former Apple employees, to add technology to cars. First product was a $500 aftermarket backup camera.

- Raised $50MM. Investors: Venrock, Accel.

- Overpriced product with lower priced substitutes, and now coming standard on increasing number of cars. Ended up not disrupting the market with any groundbreaking technology.

Food

In 2013, food looked like the next big industry to be disrupted, but it quickly became a bloodbath. My take on the fundamental problem: substitutes for food startups are many – cheap fast food, large numbers of restaurants (that are often owner-operated so present stiff competition in prices), large companies like Uber and Amazon flexed their massive advantage in distribution. Ultimately buyers weren’t willing to pay more for a modicum more convenience – people expect a lot for $15 per meal.

Meal kit companies

- Fundamentals:

- Low retention: it’s just not a great solution for how to feed yourself. Limited menu selection, steeper prices than grocery store buying (especially with decreasing cost of grocery delivery).

- Also: Low brand loyalty, harsh competition from well-funded competitors.

- Distribution into grocery stores invites your enemy to know more about you and creating private label meal kits. With large bargaining bower, they also push for steep discounts.

- Chef’d

- Meal kits without subscriptions

- Had some distribution traction with pharmacies in NYC

- Founded 2013. Closed 2018.

- Raised $40MM. Investors: Campbell Soup

- Dinnr

- [Smaller UK company, put here for good postmortem points.]

- Surveys gave deceptive early traction. When launched, they had a small fraction of orders. [Your MVP must mimic real sales, not just verbal commitment to buy.]

- Why the discrepancy? 1) People want to make you happy and don’t want to be negative; 2) People are too optimistic about their future behavior. Aspirations are fun to entertain until they’re forced to pony up money.

- “There never was a need for a service like ours. I deluded myself in thinking that there was, because I was eager to start my own thing and thought that this was something that I myself would use.”

- Stress test your ideas with a partner. Avoid unproductive advice like “I would never use this, so it won’t work.” Get more meta commentary: “how did you conduct your market research? Did you ask them to pay outright? Why do you think it’ll work here, just because it works in Sweden – what are the differences that make it work there? What are your assumptions about the customer’s problem?”

- Expect results faster and attach consequences to goals not reached.

On-demand food, vertically integrated

- Fundamental: Operations are tough, margins are thin. Easy lower cost substitutes that are tastier – restaurants, delivery, meal kits.

- In essence, these companies were “restaurants that deliver.” The technology and economies of scale didn’t materialize.

- August Capital: “estimated it takes about $12.50 to deliver a single meal on time in most U.S. cities. ‘It has become obvious that you can’t make money on individual deliveries; the cost of a single meal is too low to hide your associated fees. Who wants to subsidize a company with no path to profitability?’”

- Bento

- Raised $2MM. Investors: Jason Calacanis, Slow Ventures.

- Founded 2015. Closed 2017.

- “As it turns out, the company was paying $32 to make and deliver bento boxes being sold for $12.” After cost-cutting, “We got to, like, positive a penny.”

- Sprig

- Higher end, on-demand meals.

- Raised $57MM. Investors: Greylock, Social Capital, Accel

- Founded 2013. Closed 2017.

- Was losing $850k monthly, couldn’t expand into other cities

- HN discussion.

- Greylock partner: “It’s going to be a lot like Uber, where it’s going to be hard to imagine all that friction and inefficiency in the industry before. I think we’re changing the proposition of food.”

- Spoonrocket

- “Sub-10 minute delivery of sub-$10 meals.”

- Raised $14MM. Investors: Foundation Capital, Y Combinator, Sherpa.

- Founded 2013. Closed 2016.

- Launched with $6 meals (heavily subsidized by VC). To make economics work, raised prices to $8 and added $2.50 delivery fee (to sidestep the sub-$10 promise).

- Had early success with Bay Area college student. Struggled to scale up to SF and SD.

- Product dissatisfaction: limited options, sell out, some food quality issues (“frozen food quality”.

- Reasonable Yelp reviews at 3.5 stars.

- Eventually said it reached “positive contribution margin” but with overhead, investors weren’t willing to fund.

- Maple

- Founded 2014. Closed 2017.

- Raised $29MM. Investors: Thrive, David Chang (Momofuku), Andy Dunn.

- Gross margins were 2% (30 cents per meal) in March 2016. Forecasted loss of $16MM on revenue of $40MM. Useful financials.

Home cooks share meals, or host dinners, or private chefs cook in-home dinners

- Scarf shut down by regulation (Alberta)

- Josephine shut down by regulators (Oakland). Kapor Capital

- Kitchensurfing. Tiger Global, Spark, Union Square Ventures

- Problems with insufficient critical mass.

- Hard to retain cooks. Not as profitable or easy as thought.

- Good coverage

Meatless Products

- Not yet failed, but looks in trouble.

- Raised $220MM. Peak valuation: $1.1 billion. Investors: Khosla ventures, Li Ka-shing, Marc Benioff.

- What got it off the ground: Charismatic founder who “looks like a leader,” mission of reducing environmental and ethical impact of eating meats, a pitch of a technology platform analyzing plant proteins molecularly and using ML to replace animal products.

- Troubles

- Contractors were tasked with buying Just Mayo from stores and inflating sales numbers, which were then used to present a rosier picture to investors. Could have reached over $1MM in false sales.

- Financials presented to investors were already inflated – presented $28MM in revenue in 2014, but was actually on pace to have less than $4MM in sales, and was losing $2MM a month.

- The tech platform turned out not to yield much. A lack of plant data meant ML wouldn’t work well. Their Just Mayo was built with pea protein, a common vegan ingredient.

- Food safety issues caused Target to pull Just products.

- The company’s entire board resigned in 2017.

- New product lines delayed by years.

Misc

- “DoorDash spends more than $200 recruiting each delivery driver.” NYT

Education

- Online tutoring platform.

- Founded 2010. Acquired 2014 by Wyzant.

- Raised $2MM. Investors: Y Combinator, Sequoia.

- Founder: too dependent on SEO, which at first worked great. “That success was also a trap. It convinced us that there had to be another channel that would perform for us at the level of SEO.”

- Tried PPC, deals, partnerships, craigslist. “The acquisition costs through those channels were significantly higher than what was allowable based on our revenue per customers.”

- Panda update: “Then, in March of 2013, Google cut the ground out from under us and reduced our traffic by 80% overnight.”

- Aftewards: “We simply couldn’t find a way to generate enough leads, no matter the price. In the end, that calculus applied to nearly every paid channel we could identify.”

- The Airbnb false analogy.

- “We had modeled ourselves on AirBnB, believing we were a clear parallel of their model for the tutoring market. What we were seeing in terms of user behavior, however, was fundamentally different. Parents simply didn’t trust profiles and a messaging system enough to transact at the rate we needed. Our dropoff was too high, and the number of lessons being completed was too low.”

- “We called the new model Agency as we pulled in aspects of a traditional agency’s hands on approach. Within a month of the change, we doubled revenue. Six months after the shift, our revenue had increased another 3x and we’d increased margins from 15% to 40%.”

- Made educational apps for K-5 kids. Based in Mexico.

- Raised $36MM. Investors: 500 Startups

- CEO had committed fraud, mismanaged funds. Had inflated data about downloads and sales metrics.

AR/VR

Blin.gy/Chosen

- Chosen was American Idol on the phone.

- Raised $10MM. Investors: Ellen Degeneres (who promoted on her show)

- Pivoted to AR app Blin.gy which basically makes any background be a green screen. Marketed with Musical.ly creators, which drove 1MM installs at less than $0.10 per install.

- But tech wasn’t seamless – required a background detection step to improve quality – so users had low quality videos. Closer to 25% d1 retention.

- Running out of money. VCs: “Really great technology and vision. But how does this become a platform?’

- Useful takeaways from founder’s postmortem

- Put ALL your effort into quickly cracking the retention code. Buy as few users as possible to get the minimum necessary data to reach statistical significance to project future performance metrics. Aim for 40% d1 and 20% d30.

- Make sure you’ve built an application that is charting with high retention metrics BEFORE you give away any equity or pay for what you hope to be a large scale funnel. Your top-line installs are not important whatsoever if you did not build a better mouse trap to retain users.

- The bigger the celeb or distribution partner, the worse their conversion rates per follower are going to be.

Media/Entertainment

GigaOm

- Technology, startup media company. News, analysis produced by independent analysts. Aimed to become a platform for independent analysts to reach a wider audience.

- Founded in 2006 (founder/blogger Om Malik joined fulltime then). Closed in 2015.

- Raised $22-40MM (including debt). Investors: True Ventures.

- Conjecture: Company was running at a loss for years, taking on debt to fuel growth. It tried to monetize its products (research, events, ads) but had aggressive revenue targets it couldn’t hit. The last round of funding was used for debt service. Ultimately a balloon payment on debt to SV Bank came due, forcing a shutdown [which makes sense, given GigaOm’s sudden shutdown instead of ramping down to a more sustainable smaller business.] Recode

- Research product was aimed to be low price at $80/year, rather than the thousands by a Gartner-type. Wanted to be disruptive and try to make it up in volume. Later had to adjust pricing up to focus on enterprise and white papers.

- Annual revenues estimated at $15MM. 60% of that was research, but that wasn’t profitable (high expenses from sales).

- No postmortem from founder yet. Some takes:

- Pressure to grow quickly meant spending everywhere – growing editorial, research, sales, technology.

- Competitors like Business Insider and other startups providing research put on pressure.

- Valuation was too high for natural acquirers.

- In their last round, they should have cut burn rate immediately, instead of betting on letting growth solve the problem. Its failure was surprising because it didn’t act like anything was wrong.

- Its principles of not chasing page views, cheap headlines, and self-promotion stifled its growth, which its venture funding necessitated.

- Gaming company, built Crackdown (a success) and APB (a failure)

- Raised $83+MM. Investors: NEA.

- Had no business model around how to monetize game. Was in weird hybrid of upfront pay and microtransactions.

- Took too long (5 years) to release APB. Market had changed by then.

- “Accept that a massive budget for a single game in a single company is, more likely than not, going to kill that company”

- Player reviews:

- “In the end the game just didn’t have a population to support a PC-only title. The MMO rush that the 2000s experienced due to WoW was slowing down by 2010, and spending over 100 million in cash and 5 years of time and expecting some sort of blockbuster release on a PC only platform with zero notoriety like Blizzard was incredibly foolish “

- Glitchy, unbalanced, slow development cycle.

- [Not well-known, but put here for its good postmortem by founder and resemblance to HQ Trivia, currently going through its own problems]

- Interactive game shows – players answer questions, win prizes, live chat.

- Content is hard

- “Producing quality content every day is a herculean task, especially live. The idea of creating both the content and technology for PlayCafe seemed achievable, but TV networks focus on distribution and studios on production for good reason: both are hard.”

- “Content is an order of magnitude harder than technology with an order less upside; no YouTube producer will earn within a hundredth of $1.65 billion”:

- Marketing requires constant expertise.

- “I no longer think marketing is something smart novices can figure out part-time. As the web gets super-saturated, marketing is the difference-maker, and it’s too deep a skill to leave to amateurs.”

- [Bezos argues don’t focus on marketing, make your product great and it’ll market for you.]

- Social music experience. Users can play music live in room, and people can join and chat.

- Founded in 2011, Shut down in 2013.

- Raised $7MM. Investors: Union Square Ventures, FIrst Round

- “I didn’t heed the lessons of so many failed music startups. It’s an incredibly expensive venture to pursue and a hard industry to work with. We spent more than a quarter of our cash on lawyers, royalties and services related to supporting music. It’s restrictive. We had to shut down our growth because we couldn’t launch internationally. It’s a long road. It took years to get label deals in place and it also took months of engineering time to properly support them (time which could have been spent on product).”

- DMCA provision: “non-interactive” online radio services to operate without needing to individually negotiate licensing deals with individual labels

Social

- Twitter-like product, messages up to 256 characters. Wanted to be a platform for third-party applications. Promised ad-free.

- Raised $3MM. Investors: Andreessen Horowitz (A16Z)

- Found the virtuous cycle hard to build. Not enough users -> not enough developers -> not enough value -> not enough users.

- Location-based photo app. Photos taken are shared publicly with people nearby.

- Founded 2010. Acquired 2012 by Apple for $2-7MM.

- Raised $41MM pre-launch. Investors: Sequoia, SV Bank.

- Founders had previously been successful with previous companies, and investors were looking for the next big social app.

- Used a web 1.0 playbook – bought domain Color.com for $350k, thought first-mover advantage was big, market aggressively to users. Failed to recognize that in the 2010’s, the decreasing barrier to entry meant a “launch fast-iterate” model worked better.

- The product just wasn’t good. App received mixed reviews. Its location-based nature meant a vicious cycle where low adoption caused a poor UX (“ghosttown”). Confusing purpose for new users.

- Controversy during wind-down.

- [Lesson that models that worked in previous eras may not work again.]

- Allowed everyone to have an “ask me anything” page. Can also ask questions of people anonymously. Meant to have honest sharing conversations with friends.

- Funding: $14MM. Investors: Redpoint, SV Angel, Kevin Rose.

- Had big early success – first billion questions, lots of users.

- Anonymity caused bad behavior. 2011 bullying controversies (common thread for anonymous social apps). Lot of content was bad, sexual. In retrospect, they should have tried to degrade anonymity (but this was their golden goose).

- Growth stalled, and they tried to reinvigorate it with large features that flopped – photo handling, addon button. Could have focused more on what they knew best.

- [Small company, included here for its good user behavior postmortem]

- Share your interesting plans with friends. Facilitate serendipitious get-togethers and knowledge of cool events. Get friends to join you on your events.

- Funding: seed funding.

- Sharing frequency of plans is low, unlike Facebook status updates. Users don’t build a strong daily or weekly habit of posting, so consumers of the plans get even less value.

- “Many Plancast users don’t have any interesting plans on their calendars.”

- People want to discover interesting events less than the company thought. Many want to conserve their free time.

- Not clear incentives around sharing. What do posters get in return?

- On Facebook, Instagram, etc you get social validation. Dopamine high from likes and shares.

- Only some plans are really cool and gain social currency. And the best ones are exclusive, and not appropriate for sharing.

- As a poster you also want friends to join you on plans, but many viewers don’t want to commit to a plan in case something better comes along.

- Users became aware of events but didn’t feel necessarily welcome to join without a personal invitation. Thus the most engaging events were open in principle, like conferences or concerts.

- Plans are ephemeral, so consumption value is limited. Contrast to Facebook photos.

- Very local – friends in other areas can’t participate in events.

- Discover new content, personalized to your interests and crowdsourced ratings. Press stumble button to get new pages, then upvote/downvote. Like “I’m feeling lucky” button.

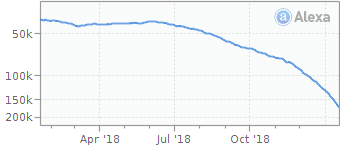

- Started in 2001, acquired by eBay in 2007, bought back by Garrett Camp in 2009, shut down in 2018.

- Fundamental: was popular for a time, but seems fell out of favor for next generation content discovery: Facebook, Reddit.

- One-step video publishing tool, drag and drop. No account required.

- Funding: $9MM. Investors: NEA, Upfront, First Round.

- Became top 1000 Alexa site.

- Hard to kick off virtuous cycle. Smaller platforms don’t get dedicated ad deals, which doesn’t monetize creators as well, which keeps viewers off, which keeps platform small.

- Less tracking of user data (because of no account requirement) meant lower ad rates.

- Video storage and bandwidth costs did not go down as quickly as expected

- Video competition from large platforms – Facebook started prioritizing its own video player, stifling Vidme social traffic.

Yik Yak

- Local anonymous message boards. Especially popular on college and high school campuses.

- Funding: $74MM. Investors: Sequoia, General Catalyst.

- Grew to be

- Big controversies around bullying. Ultimately may have been just a small fraction of the userbase, and not a major dealbreaker for majority of its users.

- More commonly reported by users:

- Introduced mandatory handles to de-anonymize people, presumably to reduce toxicity and pave way for targeted ads. Pushed engagement to connect to real life. This was antithesis to the original anonymized purpose of the app. They dialed it back to optional, but lost trust of some users.

- Seasonality of education (people are away for summer) killed engagement. Made worse when app prevented people from posting when you weren’t in the location. When people returned in fall, they moved on.

- As part of a “grow first, figure out money later” strategy, it dropped users before it could generate revenue to survive. (anonymous app Whisper is still alive, though not in hyper growth any longer)

- Fundamental: local + anonymous was an interesting experiment, but has engagement problems and invites toxicity.

Fin Tech

- Serve mid-prime borrower, a segment of small businesses without access to bank financing. Company believed they could better assess risk, and give borrowers better than merchant cash advance (give loan in exchange for % of transactions).

- Founded in 2012. Closed in 2016. Then reopens in 2018.

- Raised $70MM (partially debt).

- Found that their target borrowers had bad habits, taking on MCA loans that then drove them into default.

- They found themselves moving back to prime segment, which lowered yields and made them the same commodity as others.

- Founder wrote a post-mortem book (I haven’t read it). Quotes from interview:

- “I think at our peak, we were around $7, $7.5 million per month and that was sort of a long slog all the way through and I think others serving this mid-prime market where the loan sizes are a bit larger and the underwriting is a bit lengthier and more judgmental than automated have the same experience where there was really no magic bullet to scale the assets we were originating.”

- “I think we combined this sentiment of we need to get to a relative amount of scale to stay relevant in the industry when there’s 300 other guys that are doing the same business, but we didn’t have the capitalization to support that growth and so ultimately, I think we just bit off more than we could chew and it became more than I was capable of managing effectively. But if you look at the guys who are out there who have made it, most of them had early in their business significant financing on the equity side and most them on their second raise, on their Series B had raised well over a $100 million of equity.”

- “And I think the fintech folks, certainly some of them who are newer to the business, either couldn’t have landed that capital or didn’t quite understand or realize how much capital you needed. “

- Fundamental: the market rates for non-prime borrowers exist for a reason, and think twice before you think you can optimize your way out of it.

Loyal3

- Originally, let consumers buy IPO shares at banker prices (eg Square). Vision to democratize the investing process.

- Charged the companies fees, the pitch being that consumers will become loyal customers-investors.

- Raised $51MM.

- Their IPO deals dried up, and they pivoted to a discount brokerage, making it easy to buy shares and fractional shares. Example video

- Companies may not have seen enough value in offering allocations to their customers.

- This didn’t seem to be enough – Robin Hood, with real-time stock and ETF trading for all equities, was a better offering than Loyal3’s 75 stocks with batch trading.

- Social payments, collecting payments for friends and crowdfunding for things like parties.

- Founded 2012. Acquired 2017 by Airbnb for reported $50MM.

- Raised $62MM. Investors: Andreessen Horowitz (A16Z), SV Angel, Y Combinator.

- Good user growth through virality.

- Founder Beshara said to be charismatic and “read as a visionary.” Example interview

- Also launched Crowdhoster, used for crowdfunding (Soylent launched here).

- “User growth disguised it, but Tilt was stuck in a strategic gray zone. For many-to-one payments, it was losing to Venmo. For larger-scale crowdfunding beyond the user’s immediate social circle, it was losing to GoFundMe, Indiegogo, and Kickstarter. And for more professional ticketing operations, it was losing to established specialists like Eventbrite and Splash.”

- Founder: “Once Tilt becomes this mainstream, seamless tool, you use it when you start thinking about pooling resources, the use cases become unlimited. That’s what’s exciting about providing the platform, a tool similar to Tilt. It unlocks behavior and ideas.”

- Revenue was not a top priority – trusted with user growth, they’d figure it out there. Revenue was still in 6 figures at sale.

- Founder was said to be distracted, with a “focus on culture and creating this nirvana of a company.”

- “Tilt had decided not to build significant portions of its own processing infrastructure, instead relying on providers like Stripe, its software was of little value beyond the group-payment capabilities.”

- A personal finance manager, like Mint (its main competitor)

- Started 2005, closed 2010.

- Raised $5MM. Investors: Union Square Ventures.

- Mint launched in Sept 2007, won TechCrunch conference. In 2009 Mint was acquired by Intuit for $170MM, while Wesabe shut down a year later.

- The former CEO cites two reasons for losing:

- Didn’t work with Yodlee, an automatic financial data aggregator (eg from banks). Mint used them and had a much easier UX. Wesabe built their own, but were too slow.

- Mint made the UX frictionless as possible – automatically categorizing steps, reducing fields in signup forms. Wesabe prioritized tools that would help people improve their financial behavior. So it was helping people edit data easier, vs not having to edit at all.

- You need to make your users happy as quickly as possible, then help them improve their lives.

- “Changing people’s behavior is really hard. No one in this market succeeded at doing so.”

- Even Mint’s claimed user benefits matched national averages, especially during the recession when everyone cut back.

- Short-term, unsecured personal loans online. Aimed to build better automated risk assessment

- Default rates of about 50% in the beginning

- Total funding: $158MM. Investors: Accel, Greylock. Peak valuation, $1B.

- Effective APR of 1509% criticized (APR not great for short-term loans anyway)

- PR mess around hard-pressed borrowers unable to gain credit elsewhere. Customers were attracted in ease of getting funds, but found it hard to pay back and had to get loans from elsewhere. Guardian

- UK Regulation in 2014 tightened operations of payday loans with FCA – capped charges, limited rollovers, increase affordability checks. Also sought redress to customers for past practices, example

- Debt collection controversy: sent scary letters to customers in 2010 accusing them of fraud and threatening to involve police; sent letters from fake law firms threatening higher fees.

- Fundamental: Automated risk assessment didn’t work as well as hoped. Buyer behavior promoted unplanned rollover of and spending out of means, rather than super tight fiscal control and legitimate use of funds to get back on track. Risky practices increased PR scrutiny and regulation made practices financially unsustainable.

Misc

- Q&A service, mainly for mobile. Answered questions like “how many books are in the bible?” at a time when search engines weren’t great at that. Would also store results for SEO.

- Founded 2006, shut down 2017.

- Raised $96MM. Investors: Bezos.

- At its peak, had $21MM in annual revenue.

- Google updates improved ability to parse questions, and lowered Chacha’s search rankings.

- Reading platform for sharing notes on ebooks with friends and discussions. Business was analytics for publishers on reading behavior.

- Could not find sustainable model. Ultimately acquihired by Dropbox.

- Similar site Goodreads still exists.

Healthcare

- Personal health assistant. Users get review of insurance, help in resolving problems related to billing, recommendations for medical care. Memberships cost $20 for individuals and $50 for family.

- Raised $5MM. Investors: Social+Capital, Mayo Clinic.

- Failing to find an appropriate product market fit. Lack of focus – concierge services across all disease states, all sorts of payment structures.

- Business wasn’t figured out – who would pay for this? Consumer healthcare is tough.

- Had misalignment with investors and strategic partners on where company was going.

- Tried to force too many Mayo assets into the product, wasted time.

- Leads to muddled vision, as opposed to force of will founder who says “this is what I want to do, thanks for your advice but no thanks.”

- Waited too long before getting it in front of people.

- Venture arms of healthcare orgs (like Kaiser, Mayo) aren’t necessarily aligned with the parent org.

Caresync

- Software for chronic disease management, care coordination among patients, family and providers. Subscription fee for personal medical records.

- Raised $49MM. Investors: Merck, Greycroft

- Not much is given about their reason for failure (other than the obvious implication that not enough people bought their product).

- Oddity around public grants unaccounted for.

- Shut down after just a few months after release on app store.

- Founded by Dick Costolo. Fitness app with social reinforcement. Team of friends sign up as a group, each person declare wellness plan to group.

- “The thesis was, and still is, that social accountability and social motivation are the only way to get people to do the things they sort of otherwise wouldn’t do”

- Problems

- “Abstinence violation effect”- when they fail, people hide from support group, instead of turning to them for help.

- People found it hard to offer this kind of support, even to friends who have agreed to be workout buddies.

- “I had a hard time going that extra mile to log in there. I mean they had some stiff competition with Garmon and Strava.”

- Tried interventions: trainers to answer questions, encouraging chatting, postly 1-day and weekly plans. But people would just turn off notifications.

- The company could have still made money by charging people subscriptions up front, even though they likely wouldn’t use the app for long, Costolo says. But, he and his team had not interest in that business.

- “we were running against hard-wired human behavior.”

- Match cancer patients to clinical trials. Get tumor biopsies sequenced, then match smartly to clinical trials.

- Founded in 2015. Launched in 2018, closed 2 months later.

- Raised $90MM. Investors: Li Ka-shing.

- Got big names on board – NCI, MGH, dozens of cancer centers.

- Expected patients to pay $3k out of pocket. My guess: they didn’t verify buyer was willing to pay.

- “Driver has used much of its funding to build its own automated machines — one in San Francisco and another in China — to analyze patients’ tumor samples, which Driver arranges to get shipped from the hospital where patients got their initial tumor biopsy.”

- “We needed to bring on revenue a lot sooner than we did — as opposed to maybe spending as much time and resources building such a robust solution.” Built a whole pipeline.

- Raised $23MM.

- Local providers have intensive community relationships, do on the ground marketing and have referral sources. (classic local based service fragmentation, like tutoring)

- “Because home care is extremely fragmented, it’s the agencies who can establish long-lasting relationships and deliver highly-personalized experiences who ultimately win. It’s not a technology problem.”

- Regulation classified homecare workers as W2. Had to stop 1099. (Woe is me, this is bad for affordability)

- Pivoted to enterprise. Realized that health systems had little financial incentive to pay for non-medical home care

- Mental health app, $50/month. CBT techniques, live coaching.

- Raised $21MM. Investors: Mayfield, UPMC

- Ultimately wanted to sell to insurers, but started with consumers. Didn’t get enough traction with consumers, and insurance companies weren’t interested.

- Fundamental: did it have to do with outcomes?

- Comment

- “the lack of a reimbursement model for behavioral health was a huge challenge for growth”

- “finding and recruiting trained clinicians with experience in behavioral health was a massive challenge.”

- Patient portal that let patients communicate with PCP online. Built prototype for his father’s practice and tried to scale it to others.

- Raised seed. Investors: Blueprint Health.

- Doctor’s offices operate in a black box. Do not expect to change anything in their infrastructure. You can feed the blackbox, like give sales leads (ZocDoc).

- Father’s practice was unusual – he’s more willing to try new tech than others. Founder didn’t expand research to other practices soon enough.

- Doctors are hard to access. They’re constantly being sold to, and pharma spends huge money getting their attention.

- Founder should have asked father to try existing solutions first, then figured out how to differentiate from those.

- “Many of the true money-making businesses in healthcare really aren’t about optimizing delivery of primary care. Essentially, we had no customers because no one was really interested in the model we were pitching. Doctors want more patients, not an efficient office. “

- Hearing aid company – non-surgical bone conduction hearing device.

- Raised $74MM. Investors: Medtronic, Novartis, In-Q-Tel.

- FDA approved. Medicare declined to cover ”auditory osseointegrated implants”, deeming it a hearing aid (not covered) and not a prosthetic.

- Was on track for $8MM in revenue.

- “My advice to other entrepreneurs is ‘If you are going on a road, where there is reimbursement risk, don’t go on that road. Go self-pay.”

- [Still unclear to me where their revenue came from if not covered by Medicare, and why they couldn’t continue developing that.]

- Scrape online conversations about medications and diseases and help consumers make better health choices

- Raised $36MM.

- Had decent traffic. Probably couldn’t monetize. Wanted to build a product for pharma for CI, salesforce targeting?

B2B SaaS

- Raised $118MM from Andreessen Horowitz (A16Z), GV, Kleiner

- DroneDrone software – autopilot, collect and analyze aerial data software – autopilot, collect and analyze aerial data

- Software was too advanced for current hardware. They plowed money into producing bespoke hardware, but DJI hardware caught up and had internal software that was good enough

- Having too much money led to sinking money into forcing it to work, rather than patiently waiting for hardware to catch up

Moz by Rand Fishkin

- The project started as my personal blog about SEO in 2004. It evolved first into a consultancy and then, in 2007, a software company. We’ve raised three rounds of funding: $1.1mm in 2007, $18mm in 2012, and another $10mm in January of 2016. During that stretch, we’ve grown to ~$40mm revenue run rate, mid-market size for a SaaS business.

- From 2007–2012, Moz had just one product — Pro — our self-service subscription for SEO professionals. It was responsible for ~92%+ of our revenue

- [Vision of inbound marketer being a coherent role.] We called it Moz Analytics. That product took multiple years to build, and when launched in 2013, was largely a failure. It took most of 2014 to simply get the software into functional and usable shape, and much of 2015 to pay off technical debt. [They then unbundled it into separate products for SEO, social, etc]

- “Inbound marketing never really became a *thing,* at least, not in the way I thought it would. It’s a useful phrase to describe organic, earned marketing channels that work together, but it never turned into a job description or a role across the web marketing world. Social media marketers focus on social. Content marketers focus on content. Email marketers do email. And SEO professionals do SEO.”

- Late July 2016: That forecast showed Moz burning much more cash than we’d planned due to lower expectations for every product

- The primary proposal brought to the August 10th board meeting was to double down on SEO software, become profitable as soon as possible, and wind down Content + Wonk.

- We drastically underestimated the complexity of selling many products: how it dilutes brand association, impedes funnel optimization, and puts stress on product, marketing, sales, operations, customer service, and engineering teams

- Individuals and companies that need multiple functions across these channels don’t value “All-in-One” software, nor do they care if all their tools come from the same vendor. Instead, we (yeah, I’m the same way) would rather pay more, have a steeper learning curve, but get the best-in-class product for each task or function. The theory that Moz could better serve customers by having a wide breadth of good-enough features vs. being the absolute best at just one thing (or a handful) proved false.

- [Why profitable now?] Our philosophy was to do this once, do it deep, be profitable almost immediately, and never have to go through it again. [Instead of not planning for the worst case, and cutting twice]

Clean Energy

Clean Tech went through a boom and bust cycle around 2008-2012, featuring billions of dollars from VC and government and leading to large failures like Solyndra.

A great breakdown comes from Wired. Here are major points:

- Factors leading to a gold rush:

- Fear of climate change

- Increasing fossil fuel/electricity prices

- Signals that the US federal government would fund clean tech (energy bills passed in 2005 and 2007)

- Apparent disruptive technology (solar, biofuel, fuel cells)

- In solar, silicon prices more than quadrupled from 2004 to 2008. New solar panel designs made from different materials could be economically feasible.

- “There was a virtuous circle of capital moving to clean energy, and entrepreneurs moving to clean energy because there was a capital.”

- What stopped the music:

- Newly cheap natural gas (e.g. from fracking)

- “The financial models that had justified the massive investments in clean-energy sources were built on assumptions that the price of fossil fuels, in particular natural gas, would continue to rise.”

- China’s low-cost solar panel production, stimulated by government. This affects cost efficiency of all clean tech, like wind turbines.

- Technology didn’t reach projected effectiveness (algae biofuel) or cost efficiency (fuel cells)

- Silicon prices dropped by 90% due to overproduction (thus making new technologies unfeasible)

- Newly cheap natural gas (e.g. from fracking)

- “The truth is that starting a company on the supply side of the energy business requires an investment in heavy industry that the VC firms didn’t fully reckon with. The only way to find out if a new idea in this sector will work at scale is to build a factory and see what happens.”

- Solyndra spent $733 million on a second factory to try to manufacture at the required scale to make the economics work.